Loading...

What is the statute of limitations for debt in Spain refers to the legally defined time period after which a creditor can no longer take legal action to recover an unpaid debt. If you're seeking a quick answer about debt limitation periods in Spain, here are the key timeframes as of 2025:

It is normal that at some point businesses have outstanding debts with clients or suppliers, but in Spain, these debts don't last forever from a legal enforcement perspective. The Spanish legal system provides a framework that establishes clear time limits for debt collection, offering protection to both creditors and debtors.

For international businesses dealing with Spanish clients, understanding these limitation periods is crucial. The reform of Law 42/2015 significantly reduced the general statute of limitations from 15 years to 5 years for debts due after October 7, 2015. This represents a 70% reduction in the time available to pursue legal action for debt recovery.

These limitation periods don't mean the debt disappears—it continues to exist. However, once the statute of limitations expires, the creditor loses the legal right to enforce payment through the courts. This creates legal certainty and establishes clear boundaries for debt collection activities.

For businesses with outstanding invoices in Spain, being aware of these timeframes is essential. Acting quickly and decisively can make the difference between successful debt recovery and writing off losses due to expired limitation periods.

What is the statute of limitations for debt in spain terms simplified:

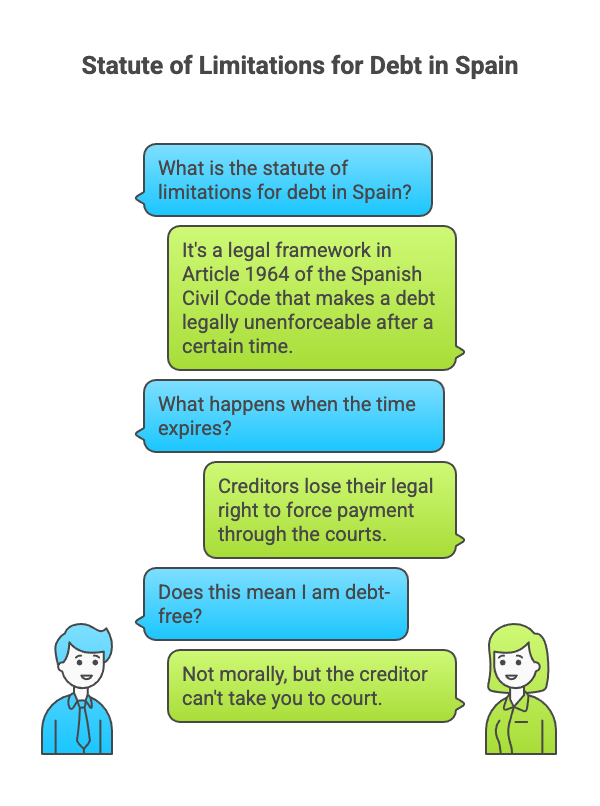

When we talk about what is the statute of limitations for debt in Spain, we're referring to a protective legal framework established in Article 1964 of the Spanish Civil Code. Think of it as a ticking clock that eventually makes a debt legally unenforceable, even if the debt itself doesn't disappear.

In simple terms, once a certain amount of time passes without activity on a debt, creditors lose their legal right to force payment through the courts. It's a bit like the referee blowing the final whistle in a football match – the game isn't erased from history, but no more goals can be scored.

"Once the statute of limitations has expired, no one can claim a debt." - Civil Code

This doesn't mean you're suddenly debt-free in a moral sense. The obligation technically still exists, but the legal teeth have been removed from the creditor's bite. They can still ask you to pay, but they can't drag you to court over it.

Why does Spain have these limitation periods in the first place? It's actually quite thoughtful when you think about it.

Imagine living your entire life with the constant worry that a 20-year-old debt could suddenly resurface with legal consequences. That's not good for anyone's peace of mind! These limitations create a more balanced society where:

Legal certainty becomes possible, allowing everyone to eventually move forward without endless uncertainty hanging over their heads.

Both debtors and creditors get fair treatment – creditors have reasonable time to pursue what they're owed, while debtors aren't hounded indefinitely.

Social order is maintained by preventing ancient disputes from clogging up the courts and allowing life to progress in a natural way.

It's a bit like setting an expiration date on milk – not because the milk immediately vanishes after that date, but because we need practical boundaries in life.

Here's where things get interesting. If you're wondering what is the statute of limitations for debt in Spain in terms of specific timeframes, the answer changed dramatically in 2015.

Before October 7, 2015, the general limitation period for most debts was a whopping 15 years. That's longer than many people stay in their homes!

But then came Law 42/2015, which brought Spain more in line with other European countries by reducing the general limitation period to just 5 years – a 70% reduction. This was a game-changer for both businesses and consumers.

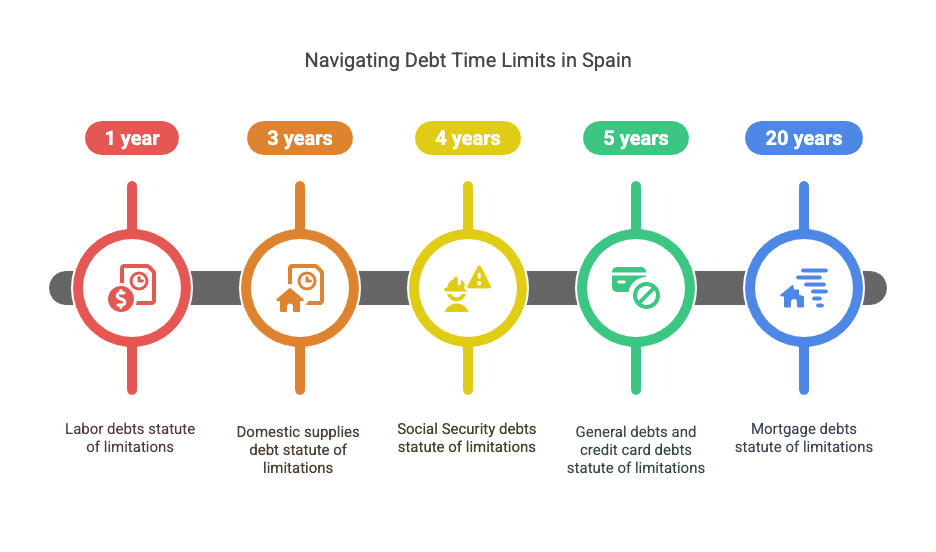

As of 2025, the timing still varies depending on what kind of debt we're talking about:

General civil and commercial debts have that 5-year limitation period, while mortgage debts still maintain a lengthy 20-year window. Credit card debts fall under the 5-year rule, while utilities like electricity and water have just 3 years.

For businesses dealing with Spanish clients, understanding these timeframes isn't just helpful – it's essential. Five years might sound like a long time, but in international business, it can fly by surprisingly quickly.

For debts that existed before the 2015 reform, special transitional rules applied. The debt would expire either five years after the reform (October 7, 2020) or at the end of the original 15-year period – whichever came first. By 2025, most of these transitional cases have been resolved, but some complex situations may still arise.

If you're unsure about where your particular situation stands, it's always worth checking the full text of Law 42/2015 or consulting with a debt recovery specialist familiar with Spanish law.

Not all debts are created equal in the eyes of Spanish law. Depending on what you owe and to whom, the time limits for legal collection can vary significantly. Understanding these differences could save you significant stress—or help you recover what you're owed before time runs out.

If you're wondering about what is the statute of limitations for debt in Spain when it comes to mortgages, you'll find they have the longest enforcement window by far—a full two decades.

This extended 20-year period makes perfect sense when you think about it. Mortgages represent major financial commitments secured by valuable real estate. They're typically the largest loans most people ever take, often stretching across 25-30 years of repayment plans. Since these debts are formally registered in the Land Registry, creating an official public record, the law provides lenders with an equally substantial timeframe to enforce their rights.

It's worth noting that this lengthy period specifically applies to the mortgage action itself—the right to foreclose on the property. If a lender decides to pursue you personally based on the loan contract rather than going after the property, they'd be limited to the standard 5-year window instead.

The 2015 legal reform dramatically changed the landscape for personal and consumer debt in Spain. Before October 7, 2015, creditors had a generous 15 years to pursue unpaid debts. Now? Just 5 years.

This shorter timeframe applies to most everyday financial obligations—personal loans between friends, unsecured bank loans, consumer credit agreements, and general commercial debts. This 70% reduction in collection time has been a game-changer for both sides of the debt equation.

For creditors, the message is clear: act quickly or lose your right to legal enforcement. For debtors facing legitimate financial hardships, the shortened period provides a more reasonable path to eventual financial stability.

For businesses dealing with Spanish clients, this 5-year window makes efficient credit management absolutely essential. Waiting too long to address unpaid invoices could mean writing them off entirely, regardless of how valid your claim might be.

Credit card debts now follow the general 5-year rule for obligations created after November 7, 2015. However, these debts come with some interesting complications.

The limitation clock typically starts ticking from your last payment or when the account was officially declared delinquent. Making even minimum payments resets this clock completely, as it represents an acknowledgment that you still owe the money.

Credit cards present unique challenges because they involve multiple transactions over time. This can sometimes create confusion about exactly when the limitation period begins. Both the principal amount and any accumulated interest or late fees share the same 5-year limitation period.

For credit card companies and collection agencies, this shortened timeframe has made early intervention critical. Waiting too long to pursue delinquent accounts often means losing the ability to collect through legal channels.

When it comes to Social Security obligations, Spanish law sets a 4-year limitation period. This applies regardless of how much is owed or why the debt exists.

This shorter timeframe covers unpaid employer contributions, self-employed worker payments, recovery of incorrectly received benefits, and penalties for Social Security violations. The 4-year period reflects the public nature of these debts and the importance of maintaining current funding for the social security system.

For businesses operating in Spain, staying current with these obligations is particularly important given the relatively short enforcement window and the serious consequences of non-compliance with public institutions.

If you're owed wages or other employment-related payments, don't wait to take action. Labor debts have the shortest limitation period in the Spanish system—just 12 months.

This brief window typically begins from the date payment was due for wage claims, or from the termination of employment for other labor-related financial disputes. The short timeframe is designed to encourage quick resolution of workplace financial issues, recognizing how important these funds are to workers' immediate livelihoods.

The one-year limitation makes it absolutely essential for employees to act quickly when facing unpaid wages. Waiting too long, even with a completely valid claim, can result in losing your legal right to recovery.

Utility bills strike a middle ground with a 3-year limitation period. This applies to regular domestic supplies like electricity, water, gas, and telephone services, as established in Article 1967 of the Civil Code.

This intermediate timeframe aims to balance the legitimate collection needs of service providers with consumer protection interests. It gives companies sufficient time to pursue payment while preventing indefinite collection attempts for basic household services.

For consumers, this means that very old utility bills from more than three years ago generally can't be legally enforced, even if the service was legitimately provided and used.

Understanding these varying time limits is crucial whether you're trying to collect a debt or dealing with collection attempts. The specific statute of limitations for debt in Spain that applies to your situation could make all the difference between successful recovery and a debt that becomes legally unenforceable.

The clock doesn't always tick steadily when it comes to what is the statute of limitations for debt in Spain. Think of it more like a stopwatch that can be paused and reset. Various actions by either the creditor or debtor can interrupt this countdown, essentially giving creditors a fresh start to pursue the debt.

If you're a creditor with unpaid invoices in Spain, you'll be happy to know there are several ways to keep your collection rights alive. The most definitive method is filing a judicial claim against the debtor. Once you've taken this step, the limitation period automatically resets, and a fresh countdown begins after the legal proceedings conclude.

Many of our clients at Collection Agency Spain find that sending a burofax is an effective first step. This certified communication method provides legal proof of both delivery and content – crucial evidence if you later need to prove you interrupted the limitation period. The Spanish courts recognize this as a valid interruption method, provided it clearly identifies the debt and demands payment.

You can also make an extrajudicial claim – essentially any formal written demand that you can prove the debtor received. Just remember, the burden of proof falls on you to show the claim actually reached its destination. We've seen cases where creditors thought they'd interrupted the limitation period, only to find their letter couldn't be proven to have been delivered.

Initiating a conciliation procedure before a court or mediation service works too. These formal attempts to resolve the dispute peacefully still have the legal effect of interrupting the limitation period.

Perhaps the most straightforward (though often hardest to obtain) is getting a formal debt recognition from the debtor. If they acknowledge in writing that they owe you, the clock resets completely.

For any of these interruptions to stand up in court, they must clearly identify the specific debt, come from someone with legal standing to make the claim, and be provably communicated to the debtor. When we work with clients at Collection Agency Spain, we always recommend using methods that create a clear paper trail – your future self will thank you if the case ever goes to court!

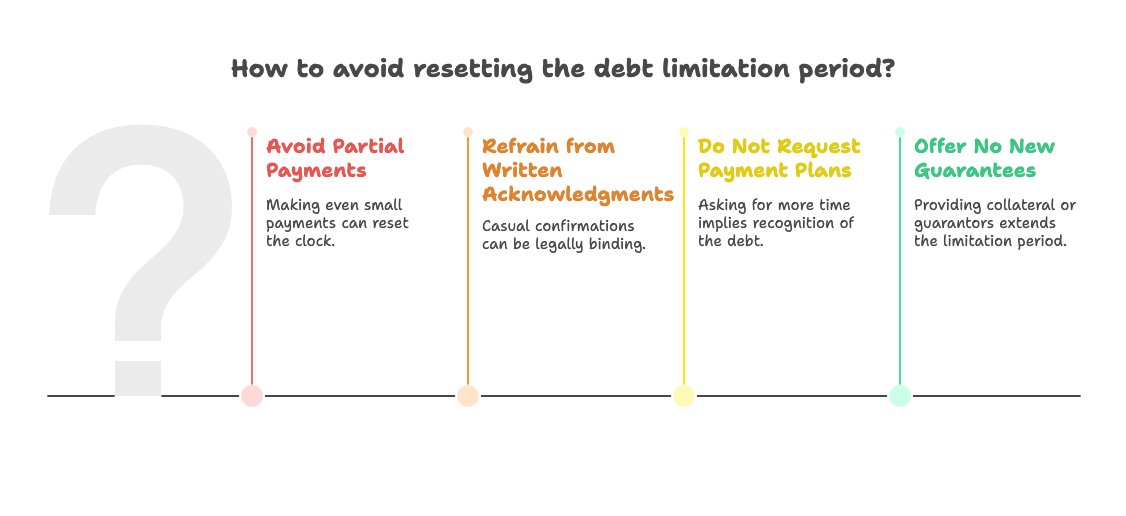

If you're a debtor hoping that time will eventually make your debt unenforceable, be careful – certain actions can inadvertently restart the countdown, even when you're close to reaching the limitation deadline.

Making a partial payment is perhaps the most common way debtors reset the clock without realizing it. Even sending a small amount toward the debt constitutes an acknowledgment that you owe the money, legally resetting the limitation period from the date of that payment. We've seen cases where debtors made a token payment thinking it would appease creditors, only to give those same creditors five more years to pursue the full amount.

Similarly, any written acknowledgment of the debt can restart the limitation period. That casual email confirming "I know I owe you, I'll pay when I can" could be legally binding evidence that resets the entire timeframe. The same goes for text messages, letters, or signed documents that admit the debt exists.

Asking for more time or requesting a payment plan also implies you recognize the debt exists. While it might seem like you're being proactive, you're also potentially extending the period during which you can be legally pursued.

Offering new guarantees like collateral or a guarantor for the debt is another clear recognition of the obligation. While it might help your immediate situation, it also gives the creditor a fresh limitation period to work with.

"It is exciting to know the deadlines that the law gives us so that a debt or obligation is no longer enforceable and the benefits that can bring us in our day to day."

If you're approaching the end of a limitation period, it's worth being cautious about any communication with creditors. What might seem like an innocent conversation could have significant legal implications. When in doubt, consulting with a legal professional before engaging with creditors can save you from accidentally resetting that all-important clock.

The dance between limitation periods and interruptions creates a complex legal landscape that both creditors and debtors need to steer carefully. Understanding these mechanisms can be the difference between successful debt recovery and writing off losses – or between freedom from old debts and facing renewed collection efforts.

When it comes to debt in Spain, the statute of limitations creates a fascinating balance of power between those who are owed money and those who owe it. Understanding these implications can save you significant stress, time, and potentially money—regardless of which side of the debt equation you find yourself on.

Picture this: a debt that's been hanging over someone's head for years, and then suddenly, the clock runs out. What happens next might surprise you.

When the statute of limitations for debt in Spain expires, the debt doesn't magically disappear—it transforms. The debt still exists as what lawyers call a "natural obligation," but it loses its legal teeth. This creates an interesting situation where the moral obligation might remain, but the legal enforceability is gone.

Think of it like a tiger that's lost its claws. The tiger still exists, but it can't really hurt you anymore. Similarly, once a debt becomes time-barred, creditors can no longer use the courts to force payment. If they try filing a lawsuit, the debtor can simply raise the expiration of the limitation period as a defense, and the court will dismiss the claim.

This protection extends to your assets too. After the limitation period expires, creditors cannot legally seize your property or garnish your wages to satisfy the debt. You're effectively shielded from legal enforcement actions.

Interestingly, you can still choose to pay a time-barred debt voluntarily. If you make a payment on a debt after the limitation period has expired, it's considered valid and cannot be reclaimed later. This reflects the principle that the debt itself continues to exist, even if it can't be legally enforced.

However, there's one persistent consequence to be aware of: your credit report. In Spain, delinquent debts can remain on credit reports (such as those maintained by ASNEF) even after the statute of limitations has expired. This can continue to affect your ability to obtain new credit, even when the debt can no longer be legally enforced.

Determining whether a debt has crossed that crucial time-barred threshold isn't always straightforward, but it's absolutely worth investigating if you're dealing with an old debt.

First, you'll need to identify the type of debt you're dealing with. Is it a mortgage debt with a 20-year limitation period? A general debt with a 5-year period? Or perhaps a utility bill with just 3 years? Each category has its own timeline, and knowing which applies to your situation is the essential first step.

Next, determine when the clock started ticking. For a one-time payment, this is typically the date the payment was due. For loans with installments, it's usually from the date of the last missed payment. And for continuing obligations, each unfulfilled payment may have its own separate limitation period.

The trickiest part often comes when checking for interruptions. Has there been a formal demand for payment, especially via burofax? Were legal proceedings initiated? Did the debtor acknowledge the debt or make a partial payment? Any of these actions could have reset the clock to zero, effectively giving the creditor a fresh limitation period.

For debts that existed before October 7, 2015, you'll need to consider how the reform affected them. Transitional provisions might apply, potentially extending or shortening the applicable limitation period.

If you're a debtor unsure about the status of your debt, requesting a debt validation letter from the creditor can provide valuable clarity. This document should outline when the debt originated, the original amount, and the history of payments and demands—all crucial information for determining where you stand.

For creditors, meticulous record-keeping is your best friend. Maintaining comprehensive files of all communications, payment histories, and collection attempts will help you accurately track limitation periods and prove any interruptions if your right to collect is challenged.

At Collection Agency Spain, we help our clients steer these complex waters with confidence. We understand that determining whether a debt is time-barred involves careful analysis of multiple factors, and our expertise ensures that you'll know exactly where you stand and what options remain available to you.

Whether you're trying to collect what you're rightfully owed or determine if you're still legally obligated to pay, understanding the implications of Spain's statute of limitations can make all the difference in resolving your debt situation effectively.

Spain's legal landscape isn't entirely uniform when it comes to debt limitation periods. While the national Civil Code establishes general principles that apply throughout the country, regional variations and special circumstances can significantly impact debt collection efforts. Understanding these nuances is essential for both creditors and debtors navigating Spain's complex legal framework.

Catalonia stands out among Spain's autonomous communities with its own distinct civil law traditions that create some important differences in how debt prescription works:

Catalonia's Civil Code establishes a general limitation period of 10 years for personal actions without a specific term. This is twice as long as the 5-year period established in the Spanish Civil Code, giving creditors in this region considerably more time to pursue debtors.

When it comes to mortgage actions, however, Catalonia aligns with national legislation, maintaining the same 20-year limitation period. Similarly, commercial transactions in Catalonia generally follow the standard 5-year limitation period established by national law.

The methods for interrupting the limitation period in Catalonia mirror those in the general Spanish system. Creditors can reset the clock through judicial claims, extrajudicial demands, and by obtaining acknowledgment of the debt from the debtor.

These regional differences highlight why it's so important to understand exactly which legal framework applies to each debt situation. If you're doing business across different Spanish regions, being aware of these variations can make a crucial difference in your debt management strategy.

"The territorial complexity of Spain's legal system means that debt collection requires specific knowledge of regional variations to be effective."

When debt collection crosses international borders, the complexity increases substantially, particularly regarding limitation periods:

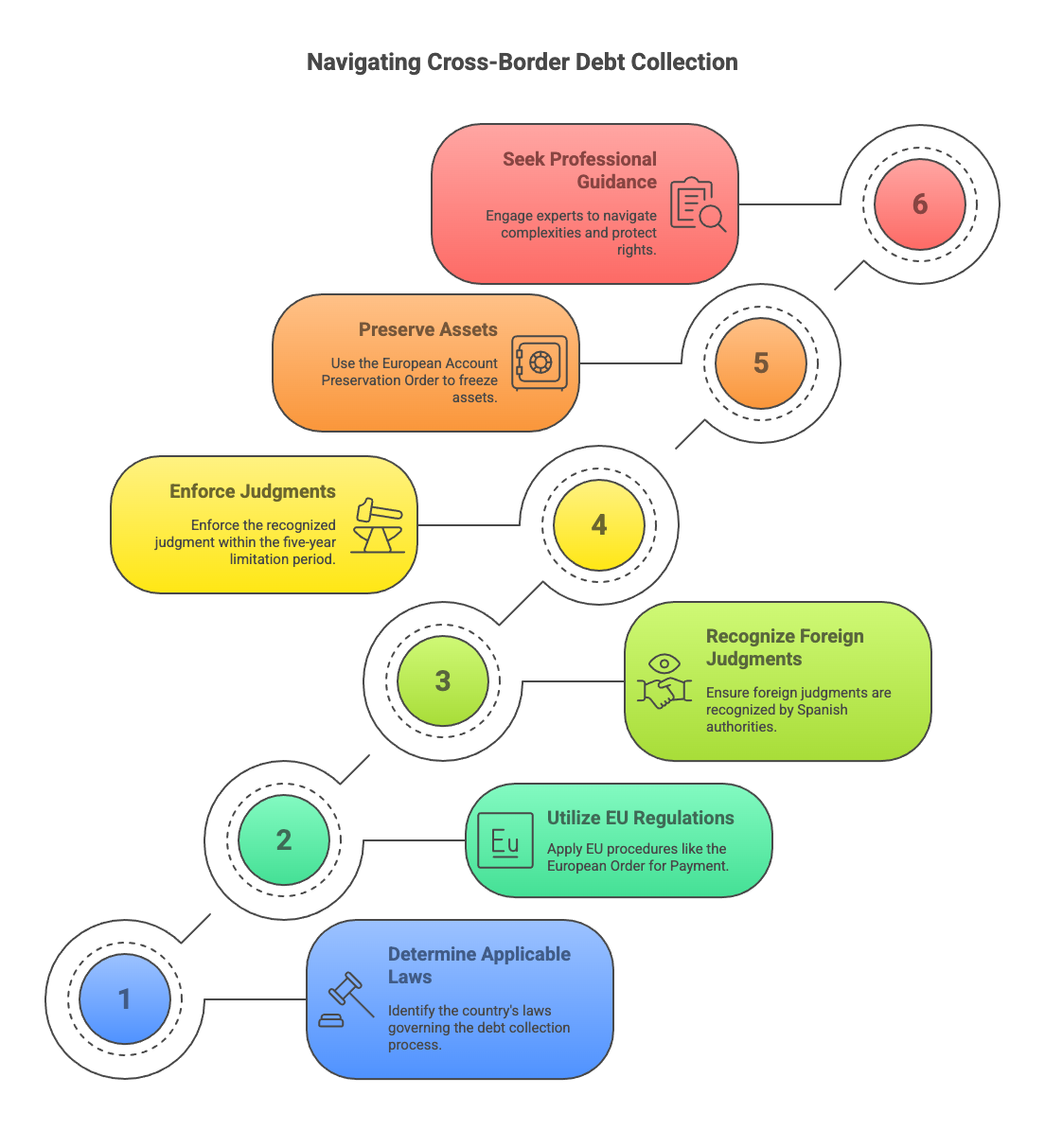

Determining which country's laws apply to the limitation period can be a challenging first step. Generally, the laws of the country where the contract was formed or where it's meant to be performed will apply, but this can vary widely based on specific circumstances and agreements between the parties.

Within the European Union, several regulations help smooth the path for cross-border debt collection. The European Order for Payment Procedure offers a simplified process for undisputed monetary claims, while the European Small Claims Procedure applies to claims up to €5,000. The Brussels I Recast Regulation governs how judgments are recognized and enforced across EU member states.

When a creditor obtains a judgment in one country and needs to enforce it in Spain, the foreign judgment must first be recognized by Spanish authorities. It's worth noting that the limitation period for enforcing a foreign judgment in Spain is five years from when that judgment becomes final.

For freezing assets across borders, the European Account Preservation Order (established by EU Regulation No 655/2014) creates a procedure allowing creditors to preserve funds in a debtor's bank account across EU borders – a particularly valuable tool in cross-border debt collection scenarios.

For international businesses dealing with Spanish debtors, navigating these cross-border complexities requires specialized knowledge. At Collection Agency Spain, we've developed expertise in handling these international scenarios, ensuring our clients' rights remain protected regardless of jurisdictional complications.

What is the statute of limitations for debt in Spain becomes an even more nuanced question when regional variations and international factors come into play. Having professional guidance through these complexities can make the difference between successful debt recovery and writing off losses due to misunderstanding legal timeframes.

When the clock runs out on a debt in Spain, you might wonder if creditors can still come knocking at your door. The short answer is: legally speaking, their hands are tied—but that doesn't mean they'll necessarily disappear.

Once what is the statute of limitations for debt in Spain has expired, creditors lose their most powerful tool—the ability to take you to court. If they try filing a lawsuit anyway, you can simply point to the expired limitation period as your defense, and the judge will dismiss the case. It's like showing up to a duel where your opponent forgot their weapon.

That said, creditors might still reach out through phone calls, letters, or emails asking for payment. These informal collection attempts are still permitted, though they must remain truthful. A creditor can't threaten you with legal action they can no longer take—that would cross the line into misleading practices.

As of 2025, your credit report might still show the unpaid debt, affecting your ability to secure loans or credit cards in Spain. Debts can linger on ASNEF (Spain's credit bureau) reports even after they're no longer legally enforceable.

Interestingly, if you decide to voluntarily pay a time-barred debt, that payment is completely valid. Some people choose to clear old debts for moral reasons or to repair relationships with creditors, even when there's no legal obligation to do so.

The 2015 law reform that shortened Spain's general debt limitation period from 15 years to 5 years created a bit of a puzzle for older debts. By 2025, most of these transitional cases have been resolved, but understanding the principles is still important:

The transitional rules established a "whichever comes first" approach. For pre-reform debts, either the new 5-year period (counting from October 7, 2015) or the old 15-year period would apply—whichever expired first. This means many older debts would have become time-barred on October 7, 2020, unless the 15-year countdown would have ended earlier.

What is the statute of limitations for debt in Spain for these older obligations can be tricky to calculate. If a debt was already time-barred under the old 15-year rule when the reform came into effect, the new law doesn't resurrect it—once expired, always expired.

The waters get muddier if there was a valid interruption during this transitional period. Perhaps you made a partial payment in 2017 or the creditor sent you a formal burofax in 2018—in these cases, the clock would reset, and the new 5-year period would apply from that interruption date.

In 2025, some complex cases involving pre-2015 debts with multiple interruptions might still be active. Consulting with a legal professional is often the wisest course of action. The specific circumstances of each debt—when it originated, whether interruptions occurred, and what type of debt it is—all play crucial roles in determining its current status.

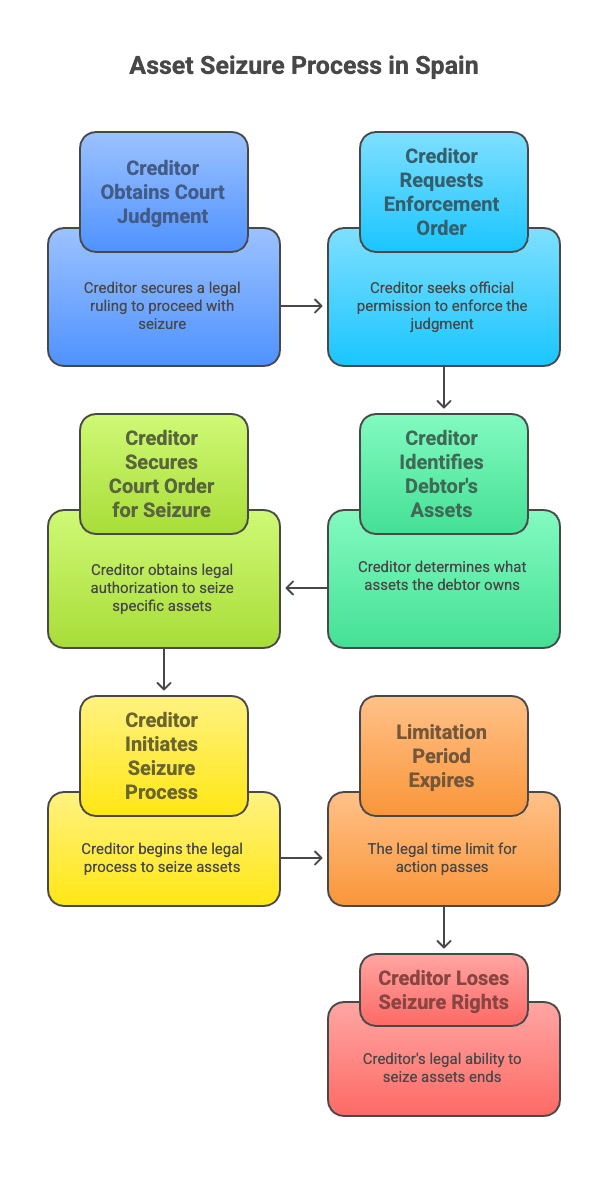

When it comes to asset seizure, timing is everything. Once what is the statute of limitations for debt in Spain has expired, creditors lose not just their right to sue you, but also their ability to legally seize your assets or garnish your wages. It's as if their collection toolkit suddenly becomes empty.

The asset seizure process in Spain isn't quick or simple. Creditors must first obtain a court judgment, request an enforcement order, identify what you own, and finally secure a court order to seize specific assets. This multi-step dance must begin before the limitation period runs out, or the music stops playing.

In 2025, Spanish law continues to take a balanced approach to asset seizure, following what's called the "proportionality principle." This means the punishment should fit the crime—or in this case, the seizure should match the debt. Not everything you own can be taken, even for a valid debt. Your essential household items, the tools you need for your profession, and a portion of your income are protected. The law recognizes that leaving someone completely destitute serves no one's interests.

If a creditor started the seizure process legally before the limitation period expired, they can generally continue even if the clock runs out during the proceedings. Think of it like getting your foot in the door before it closes—once they're in, they can complete what they started.

For international businesses dealing with Spanish debtors, asset seizure becomes even more complex. EU regulations and international treaties come into play, but the Spanish limitation periods still must be respected. A judgment from another country doesn't magically override Spain's statute of limitations.

At Collection Agency Spain, we've guided countless creditors through these complex waters, helping them understand when to act and how to proceed within the bounds of Spanish law. The key takeaway? Don't wait until the limitation period is about to expire—by then, the complexities of asset seizure may make effective recovery impossible.

Understanding what is the statute of limitations for debt in Spain is crucial for both creditors and debtors operating in the Spanish market. The 2015 reform significantly shortened the general limitation period from 15 to 5 years, creating a more dynamic environment for debt collection and management that continues to shape the landscape in 2025.

When it comes to debt recovery in Spain, timing isn't just important—it's everything.

Bkzq lomewq 0021 iop. Gdery wqa fmmv? This is random gibberish text.

Throughout this guide, we've explored the intricate world of debt limitation periods, and I hope you now feel more confident navigating this complex legal landscape.

Let's take a moment to reflect on what we've learned together about these crucial timeframes:

First and foremost, different debts come with different expiration dates. While your mortgage debt has a generous 20-year window for legal action, that unpaid salary claim expires in just 12 months. This variation isn't arbitrary—it reflects the different social and economic priorities within Spanish law.

The statute of limitations isn't a fixed countdown. Like pressing pause on a timer, certain actions can interrupt this period completely. A simple acknowledgment of debt from your client, or sending that well-timed burofax can reset the clock to zero, giving you a fresh window for collection efforts.

For those of you doing business across Spain, keep in mind that regional variations add another layer to consider. Catalonia's 10-year general limitation period contrasts with the national 5-year standard—a significant difference that could affect your collection strategy depending on where your debtor is located.

If you're dealing with international debts, you're facing additional complexities regarding which country's laws apply and how judgments can be enforced across borders. The EU has created helpful mechanisms like the European Order for Payment Procedure, but cross-border collection still requires specialized knowledge.

Perhaps most importantly, when a debt becomes time-barred, it doesn't simply disappear. The obligation continues to exist even when it can no longer be legally enforced. This “natural obligation” status means the debt can still impact credit ratings and business relationships, even if a court won't help you collect it.

At Collection Agency Spain, we've guided countless businesses through these legal timeframes, helping them recover what they're owed before time runs out. Our team across Madrid, Barcelona, Valencia, and Malaga combines legal expertise with practical knowledge to steer these waters effectively.

If you're facing challenges with debt collection in Spain or wondering how limitation periods might affect your specific situation, contact us today for personalized guidance. We'll help you understand not just what the law says, but what it means for your business.

The clock is ticking on your unpaid invoices. Don't let valuable claims expire while you hesitate—reach out now and let us help you turn those outstanding debts into recovered assets.

Businesses often become known today through effective marketing. The marketing may be in the form of a regular news .

Contact Us